Quick Read

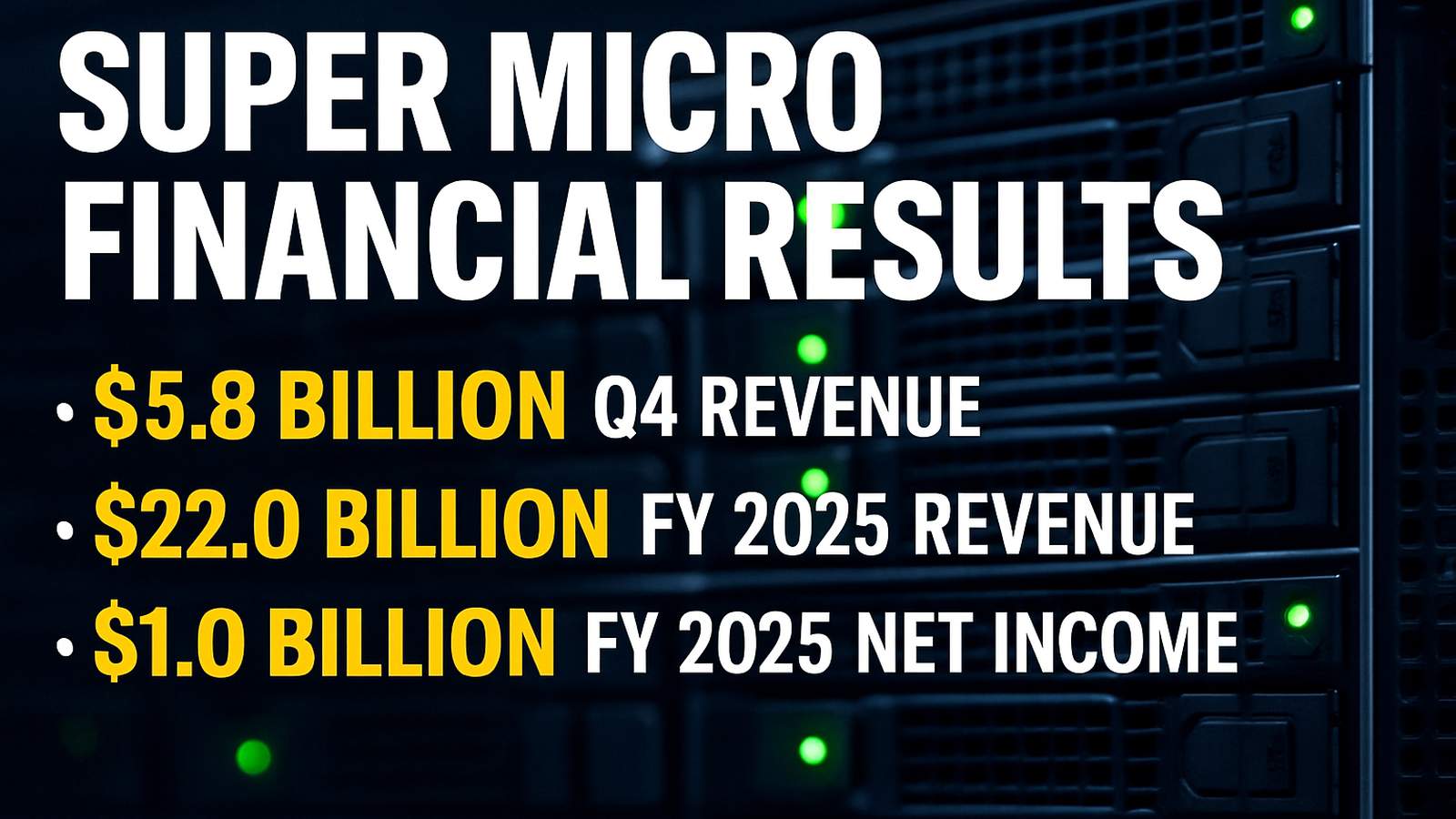

- Supermicro reported Q4 FY2025 revenue of $5.8 billion, missing Wall Street estimates.

- The company’s stock dropped over 10% following weak results and soft Q1 FY2026 guidance.

- Gross margins shrank to 9.6%, raising concerns about profitability amid competitive pressures.

- Despite short-term challenges, Supermicro projects FY2026 revenue of at least $33 billion.

- Analysts caution about valuation risks but see long-term potential in AI infrastructure.

Super Micro Computer, Inc. (NASDAQ: SMCI), a leader in AI, cloud, storage, and 5G/Edge IT solutions, announced its fourth-quarter fiscal year 2025 (Q4 FY2025) financial results on August 5, 2025. While the company showcased solid year-over-year revenue growth, its earnings and gross margins fell short of Wall Street expectations, resulting in a significant sell-off in its stock price.

Mixed Financial Performance in Q4 FY2025

Supermicro reported Q4 FY2025 revenue of $5.8 billion, marking an 8% increase compared to the same period last year. However, this figure missed analysts’ expectations of $6 billion, as reported by Economic Times. The company’s gross margin also declined to 9.6%, down from 10.2% in Q4 FY2024, reflecting cost pressures and pricing challenges in the competitive AI hardware market.

Net income for the quarter was $195 million, a decrease from $297 million in Q4 FY2024. Adjusted earnings per share (EPS) stood at $0.41, below Wall Street’s forecast range of $0.44–$0.45. These results, coupled with a weaker-than-expected margin performance, fueled concerns among investors about the company’s ability to sustain profitability amid growing demand for AI infrastructure.

Charles Liang, Founder, President, and CEO of Supermicro, emphasized the company’s achievements during the fiscal year. “We made solid progress in FY25 by growing our AI solution leadership, particularly in Neoclouds and data center solutions,” Liang stated. Despite the challenges, he expressed optimism about the company’s innovative Datacenter Building Block Solutions (DCBBS), which aim to streamline data center deployment and enhance customer value.

Stock Plunge Reflects Investor Concerns

Following the earnings announcement, Supermicro’s stock price dropped over 10% in after-hours trading, erasing recent gains. According to CNBC, the disappointing Q4 results and conservative guidance for Q1 FY2026 rattled investors who had high expectations fueled by the booming AI server market. This marked a sharp reversal for the company, which had previously been one of the standout performers in the AI hardware sector.

The market reaction underscored the heightened scrutiny on AI-focused companies, especially as competition intensifies and costs rise. Analysts from Bank of America downgraded the stock, citing valuation risks and challenges in maintaining margin expansion. The average analyst price target for SMCI now hovers between $42 and $44, down from earlier projections.

Conservative Guidance for FY2026

Supermicro provided a cautious outlook for the first quarter of fiscal year 2026 (Q1 FY2026), projecting revenue between $6.0 billion and $7.0 billion and adjusted EPS of $0.40 to $0.52. Both figures fell below analysts’ expectations of $6.6 billion in revenue and $0.59 in EPS, as noted by Yahoo Finance.

For the full fiscal year 2026, the company expects revenue of at least $33 billion, significantly higher than FY2025’s $22 billion but below its earlier internal target of $40 billion. This tempered outlook suggests a recalibration of growth expectations as the company navigates market challenges and increased competition in the AI sector.

Long-Term AI Potential Remains Intact

Despite the short-term setbacks, Supermicro remains well-positioned to capitalize on the growing demand for AI infrastructure. Its partnership with NVIDIA and its focus on GPU-based systems have solidified its reputation as a key player in the AI hardware revolution. Analysts believe the company’s innovative product offerings, such as DCBBS, and its expanding global operations will drive long-term growth.

However, the recent results serve as a reminder that even industry leaders face challenges in scaling profitably. Rising component costs, slower-than-expected client orders, and intensified competition are factors that could weigh on the company’s financial performance in the near term.

For investors, the mixed results highlight the importance of balancing growth expectations with operational execution. While the AI revolution continues to unfold, the road ahead for Supermicro may require strategic adjustments to maintain its leadership position in the market.

In conclusion, Supermicro’s Q4 FY2025 results reflect both the opportunities and challenges of operating in a rapidly evolving AI landscape. While the company’s long-term growth prospects remain strong, its ability to navigate short-term headwinds will be critical to sustaining investor confidence.